A recent headline caught my attention: "The CRE market looks to be okay unless the country experiences a significant economic downturn." It's the kind of statement that sounds reasonable until you look at the data — and then it starts to fall apart.

The problem isn't that it's wrong exactly. It's that it points investors toward the wrong variable.

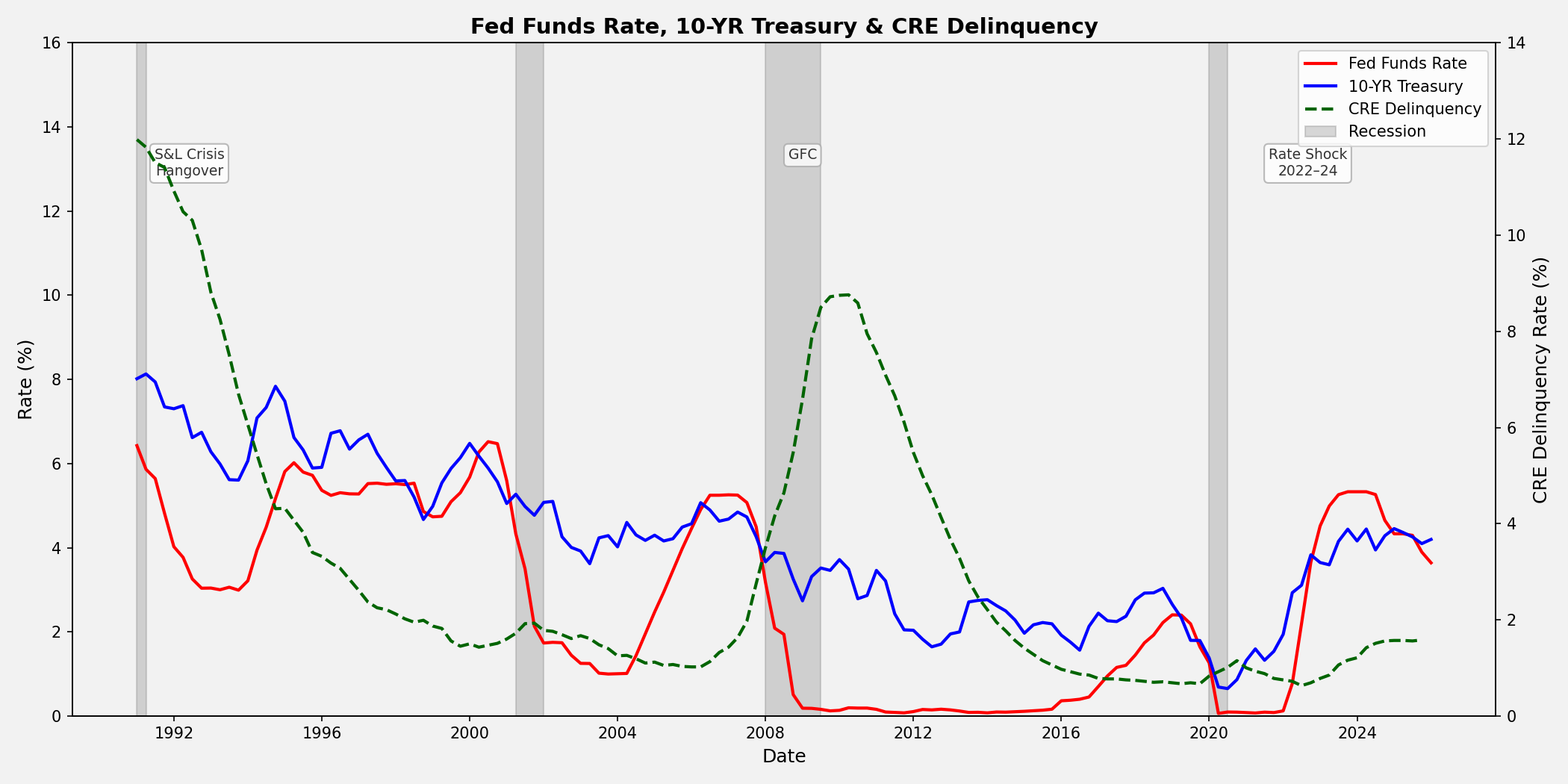

The CRE chart tells a complicated story

Over the past three decades, commercial real estate distress has not tracked cleanly with either recessions or the level of interest rates. As the chart below shows, delinquency spikes have been episodic — most dramatically in the early 1990s and during the Global Financial Crisis — and they don't coincide neatly with the onset of recessions or with peak rates. They tend to emerge with a lag, after broader financing conditions have already deteriorated.

From Federal Reserve Economic Data. (Converted to quarterly for consistency and presentation.)

The recent period makes the point vividly. The Fed raised the Fed Funds Rate by 500 basis points in roughly two years — the most aggressive tightening in four decades — yet CRE delinquencies rose only modestly. To many observers this seemed reassuring. But experienced investors recognized it differently: stress in CRE doesn't announce itself immediately. It surfaces when existing financing structures are forced to adjust to new conditions — at refinancing, at maturity, at covenant review. The clock is still running.

The practical implication for non-institutional developers and investors is underappreciated. The factors that affect NOI — rents, occupancy, operating expenses, local supply and demand — tend to be gradual, local, and manageable. The factors that affect financing — interest rates, credit availability, lender terms, cap rate movements — can be abrupt, systemic, and can change the economics of a transaction almost overnight. Both matter. Most investors spend most of their time on the first category.

Which brings us to the interest rate question

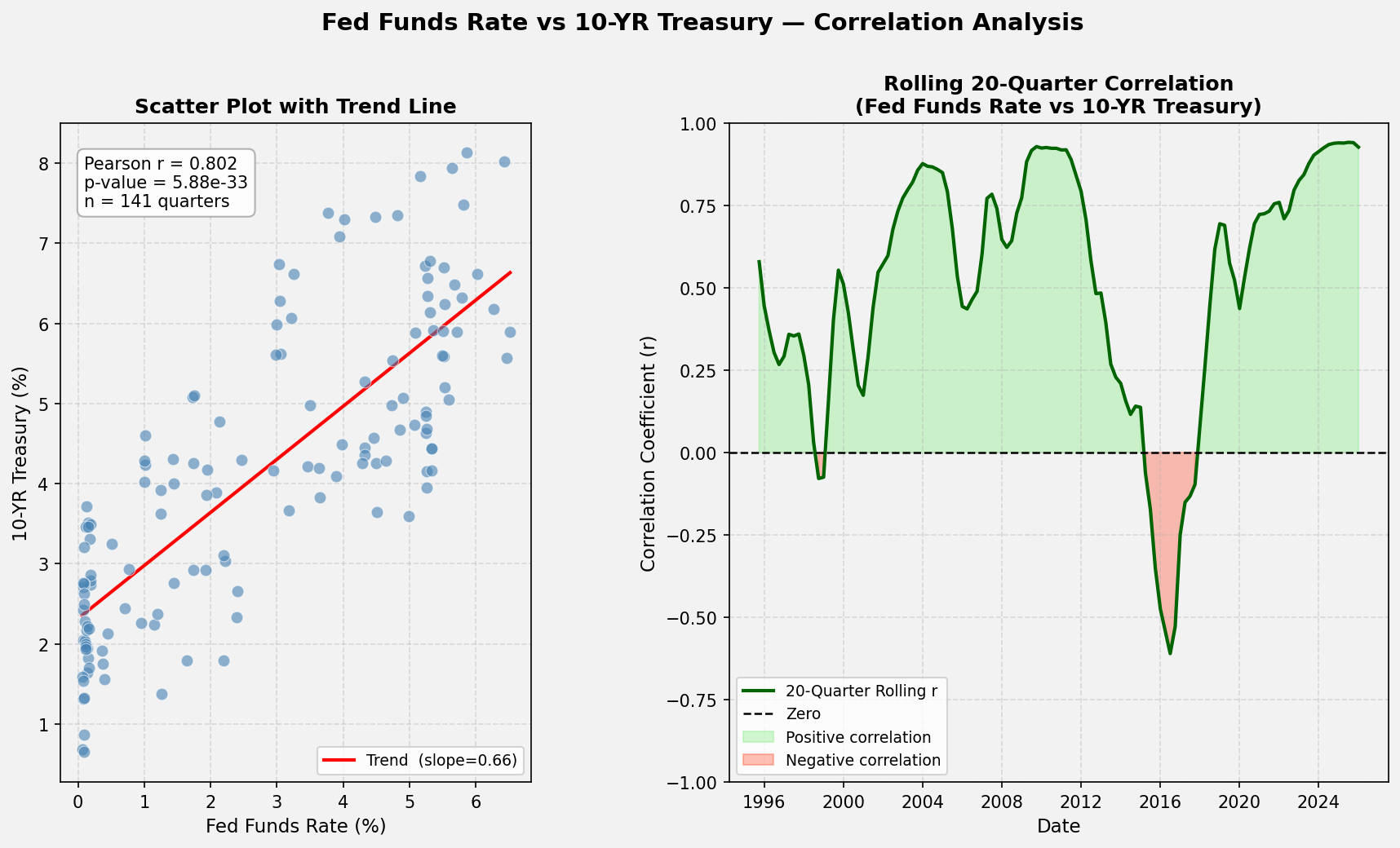

If financing conditions are what you really need to watch, then understanding the relationship between the Fed Funds rate and the 10-Year Treasury becomes essential — because it is the 10-year, not the Fed Funds rate, that directly drives fixed-rate CRE lending and cap rate pricing.

Given the way interest rates are covered in the financial press, it's easy to assume a reliable, proportional relationship between the two. The data suggests otherwise.

The scatter plot shows a Pearson r of 0.802 over the full period — meaningful positive correlation overall. But the rolling 20-quarter chart on the right tells the more important story: that correlation has varied dramatically, frequently falling below 0.50 and turning briefly negative around 2016. The overall number overstates the relationship.

The most famous illustration of this is the Greenspan Conundrum of 2004–2006, when the Fed raised rates 17 consecutive times from 1% to 5.25% and the 10-year barely moved. Markets were telling a different story than the Fed. More recently, during the post-QE normalization period, the two rates actually moved in opposite directions for an extended stretch — meaning investors who assumed Fed hikes would proportionally reprice cap rates and compress asset values were working from a faulty model.

Prof. Aswath Damodaran of NYU has argued compellingly and with considerable data that the Fed's influence over long-term market rates is substantially overstated — that the 10-year is fundamentally a market rate reflecting inflation expectations and real growth, not an instrument the Fed controls.* Our rolling correlation chart is a simple illustration of the same point.

The bottom line

Watching the Fed is not the same as understanding your financing risk. The relationship between Fed policy and the rates that actually govern CRE transactions is real but inconsistent, sometimes weak, and occasionally perverse. Moreover, interest rate is just one financing factor among many. Credit availability, terms, covenants and flexibility are equally crucial. For investors in commercial real estate — particularly non-institutional investors without teams dedicated to capital markets — that distinction is not academic. It's the difference between underwriting a deal correctly and being surprised when the refinancing environment looks nothing like what you expected when you underwrote it.

*Aswath Damodaran, "Fed Up With Fed Talk? Factchecking Central Banking Fairy Tales," September 20, 2024.